12 August 2024

Last week started with rapid drawdowns in many global equity indices, and some historic daily moves in Japan – both down and up. The VIX spiked to above 60 on Monday, a level last seen in the Covid market crisis of March 2020. And while markets regained their composure later in the week – the VIX fell back below 30 and the S&P 500 stabilised – there is still major uncertainty on how developments might pan out in the coming weeks.

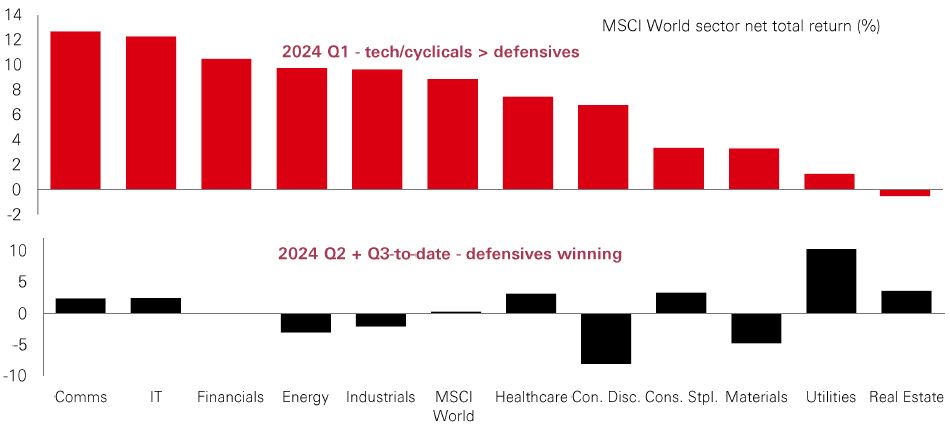

As the recession risks are now clearly higher than anticipated only a few weeks ago, we need to consider the potential for “negative feedback loops” stemming from recent market action, which can dampen business and consumer confidence. With valuations in pockets of the risk asset universe still looking stretched (mega-cap tech, global high-yield credits) we think it makes sense to be cautious.

Meanwhile, defensive parts of the stock market (consumer staples, healthcare, and utilities) could be safe harbours. And real estate – although cyclically sensitive – is helped by falling rate expectations. With uncertainty still high, defensives remain in focus.

Last week’s sell-off in global risk assets had a mixed impact on emerging markets across Asia. Much of the pain was felt in trade-dependent economies like Taiwan and South Korea, where in-demand sectors like semiconductors are sensitive to a slowdown in US growth. The region’s chipmakers have surprised to the upside on earnings this reporting season, suggesting still-solid demand for chips. Yet July’s US tech sell-off had already had a chilling effect on stock prices. From year-highs in mid-July, Korea’s Kospi index was down as much as 16% amid the volatility.

Mainland Chinese stocks have been under pressure all summer but held up better than most last week. In part that was because its stocks have relatively low overseas exposure versus global peers. There are also signs that analysts are feeling more optimistic about them, with 12-month forecast earnings picking up since early Q2. And in India, stocks experienced only mild drawdowns, outperforming regional peers despite relatively rich valuations. That was helped by recent earnings trends that have been broadly in line with expectations.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future.

This information shouldn't be considered as a recommendation to buy or sell specific sector/stocks mentioned. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way.

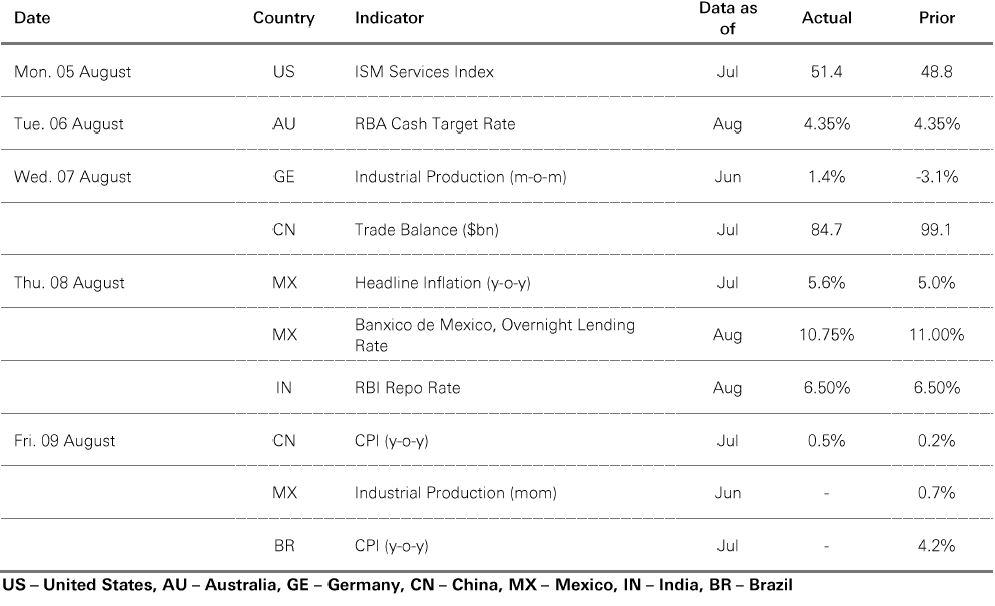

Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 11.00am UK time 09 August 2024.

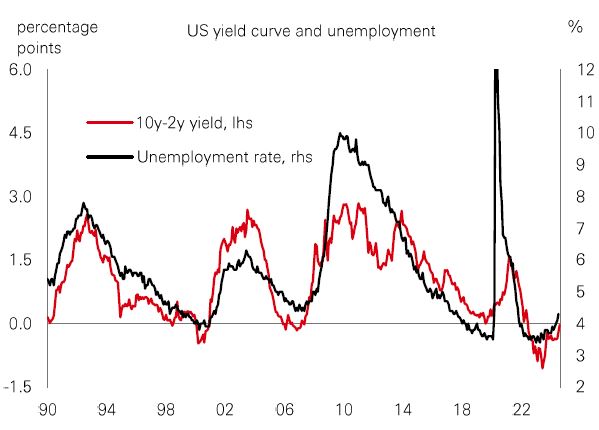

Markets have had a health scare – call the doctor! Or better, call three of them (Dr Yield-Curve, Dr Credit-Spread and Dr Sahm) who are often used to diagnose recessions.

What do these doctors say? First, the yield curve is dis-inverting via a ‘bull steepening’ (i.e. short-term interest are rates falling faster than long rates). Second, credit spreads are now rising, although not quite yet to historically concerning levels. Finally, on the real-economy side, the Sahm rule, which tracks the change in the unemployment rate, has breached a key threshold after July’s bad labour market data. While several special factors – including Hurricane Beryl – could have temporarily boosted unemployment, a wide range of labour indicators highlight the jobs market is cooling.

The US economy could disappoint overly-optimistic market expectations from mid-2024, with growth dropping below trend, which requires close monitoring.

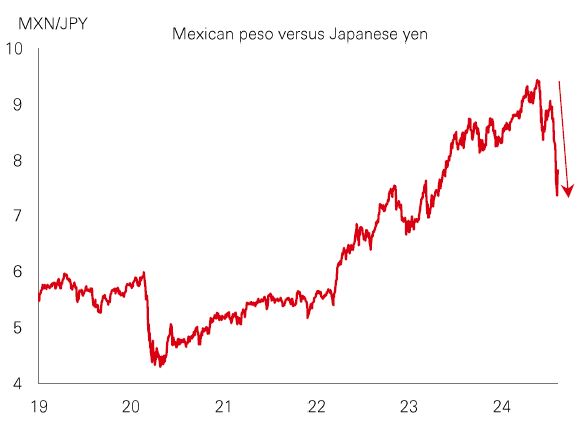

Economists have tended to focus on fundamental triggers for the market tantrum. But technical forces – especially the unwinding of carry and dispersion trades – have amplified the bad macro news, creating a major volatility (VIX) shock in markets.

Carry trades need a cheap funding currency to sell (e.g. yen) and high-yielding currencies to own (e.g. Mexico). While volatility stays low, you can pocket the rate differential. Dispersion trades sell volatility on an index (e.g. S&P 500) and buy volatility on index constituents. While correlations are low, profits follow.

But crisis dynamics weed out leveraged players. Bad macro news and rising volatility began an unwinding of these trades, and soon enough it was a cascade, amplifying volatility. In the last week, we had a vicious cycle as the risk averse are forced sellers.

What breaks the cycle? Some market stability helps. Evidence shows that most of the yen ‘excess shorts’ are now unwound. And last week’s BoJ-speak has been dovish. Meanwhile, lower numbers on the VIX and VVIX indices are welcome news. But, ultimately, global markets will remain sensitive to the US economic data-flow.

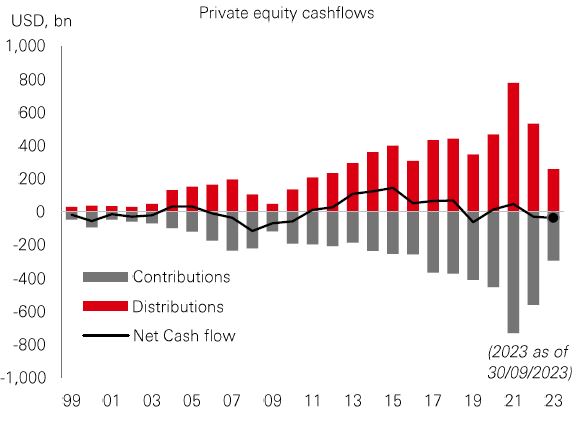

A backdrop of elevated rates and economic uncertainty has been challenging for the private equity asset class in recent years. Higher borrowing costs and a difficult environment to sell investments has meant that private equity investors have put more in (via capital calls by funds) and got back less (in distributions) – resulting in negative cash flows since 2023.

It’s a marked change from 2021, when cashflows were positive. Back then, cash calls grew on a boom in post-Covid dealmaking, and distributions back to investors surged to a high watermark of almost USD 750bn – up from USD 462bn in 2020.

Some investment specialists think that following that surge in activity, a period of relative quiet was inevitable. Consequently, industry data suggest private equity firms are sitting on more than USD 2tn of ‘dry powder’ - committed but unallocated capital. But there is optimism, as central banks face pressure to reduce rates. The prospect of a lower rate environment could help private equity dealmaking to bounce back.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. This information shouldn't be considered as a recommendation to buy or sell specific sector/stocks mentioned. Any views expressed were held at the time of preparation and are subject to change without notice. Source: HSBC Asset Management. Macrobond, Bloomberg, Datastream. Data as at 11.00am UK time 09 August 2024.

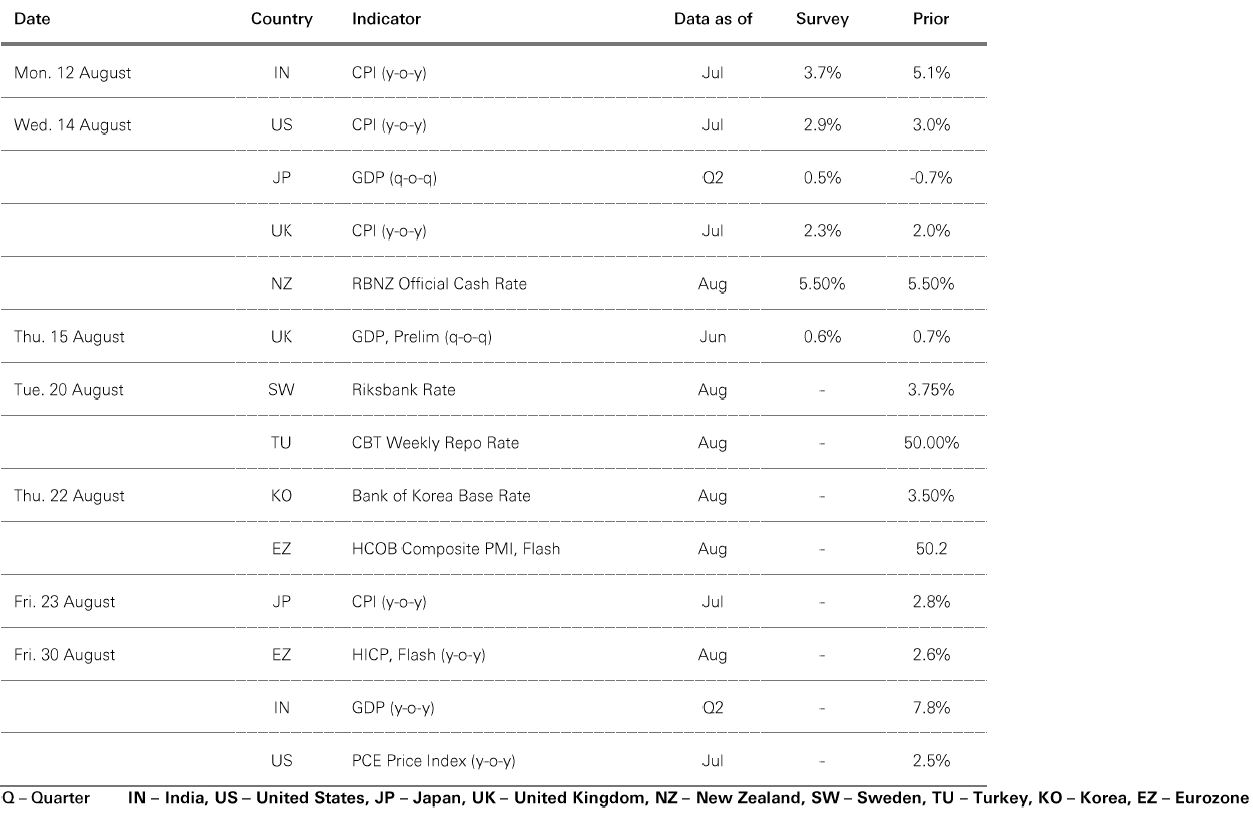

Source: HSBC Asset Management. Data as at 11.00am UK time 12 August 2024. This information shouldn't be considered as a recommendation to buy or sell specific sector/stocks mentioned. Any views expressed were held at the time of preparation and are subject to change without notice.

Global risk assets continued to sell off sharply early in the last week as July’s correction in US tech stocks evolved into a broader market rout driven by signs of faster than expected cooling in the US economy. An unwinding of yen-funded carry trades – triggered by the previous week’s surprise rate hike by the Bank of Japan – added to the volatility. The worst of the impact was felt in equities, but the S&P 500 and small-cap Russell 2000 both regained composure later in the last week. Major EM indices were more resilient, with China’s Shanghai Composite index finishing slightly lower, India’s Sensex flat, and Brazil’s Ibovespa staging a strong relief rally. In core bonds, US Treasury yields arrested recent falls to finish higher. In commodities, oil prices rose on growing supply concerns in the Middle East. Gold recovered from a mild correction early in the last week to finish with a modest decline.

This document has been issued by The Hongkong and Shanghai Banking Corporation Limited (the "Bank") in the conduct of its regulated business in Hong Kong and may be distributed in other jurisdictions where its distribution is lawful. It is not intended for anyone other than the recipient. The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document must not be distributed to the United States, Canada or Australia or to any other jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings.

This document has no contractual value and is not and should not be construed as an offer or the solicitation of an offer or a recommendation for the purchase or sale of any investment or subscribe for, or to participate in, any services. The Bank is not recommending or soliciting any action based on it.

The information stated and/or opinion(s) expressed in this document are provided by HSBC Global Asset Management Limited. We do not undertake any obligation to issue any further publications to you or update the contents of this document and such contents are subject to changes at any time without notice. They are expressed solely as general market information and/or commentary for general information purposes only and do not constitute investment advice or recommendation to buy or sell investments or guarantee of returns. The Bank has not been involved in the preparation of such information and opinion. The Bank makes no guarantee, representation or warranty and accepts no responsibility for the accuracy and/or completeness of the information and/or opinions contained in this document, including any third party information obtained from sources it believes to be reliable but which has not been independently verified. In no event will the Bank or HSBC Group be liable for any damages, losses or liabilities including without limitation, direct or indirect, special, incidental, consequential damages, losses or liabilities, in connection with your use of this document or your reliance on or use or inability to use the information contained in this document.

In case you have individual portfolios managed by HSBC Global Asset Management Limited, the views expressed in this document may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management Limited primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

The information contained within this document has not been reviewed in the light of your personal circumstances. Please note that this information is neither intended to aid in decision making for legal, financial or other consulting questions, nor should it be the basis of any investment or other decisions. You should carefully consider whether any investment views and investment products are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. The investment decision is yours but you should not invest in any product unless the intermediary who sells it to you has explained to you that the product is suitable for you having regard to your financial situation, investment experience and investment objectives. The relevant product offering documents should be read for further details.

Some of the statements contained in this document may be considered forward-looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Such statements do not represent any one investment and are used for illustration purpose only. Customers are reminded that there can be no assurance that economic conditions described herein will remain in the future. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We can give no assurance that those expectations reflected in those forward-looking statements will prove to have been correct or come to fruition, and you are cautioned not to place undue reliance on such statements. We do not undertake any obligation to update the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Investment involves risk. It is important to note that the capital value of investments and the income from them may go down as well as up and may become valueless and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Past performance information may be out of date. For up-to-date information, please contact your Relationship Manager.

Investment in any market may be extremely volatile and subject to sudden fluctuations of varying magnitude due to a wide range of direct and indirect influences. Such characteristics can lead to considerable losses being incurred by those exposed to such markets. If an investment is withdrawn or terminated early, it may not return the full amount invested. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability in certain jurisdictions. Narrowly focused investments and smaller companies typically exhibit higher volatility. There is no guarantee of positive trading performance. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Mutual fund investments are subject to market risks. You should read all scheme related documents carefully.

Copyright © The Hongkong and Shanghai Banking Corporation Limited 2024. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Issued by The Hongkong and Shanghai Banking Corporation Limited