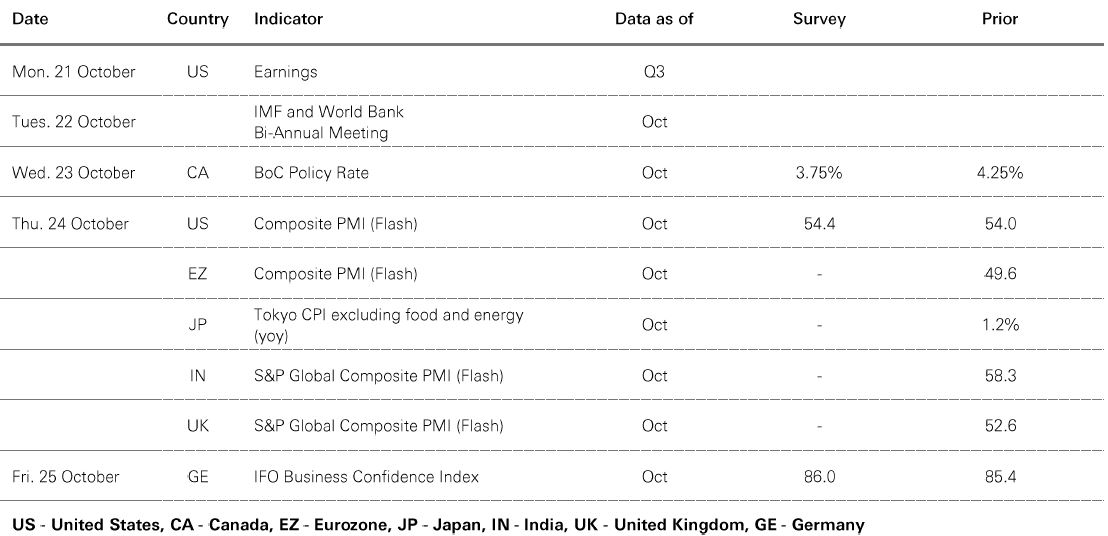

21 October 2024

After recently announcing new stimulus measures, China’s policymakers have yet to fill in the details on the scale of support planned for tackling issues in housing markets, local governments, and consumer confidence. But with recent press conferences unveiling new commitments, there is clear evidence of a fundamental shift in policy thinking.

Speculating on the precise timing of China’s stimulus isn’t sensible. However, the “three arrows” policy strategy – liquidity, fiscal/credit, structural measures – offers a way forward to boost the economy out of the deflation trap. With further policy meetings in the calendar – the NPC standing committee in a few weeks – we may hear more soon.

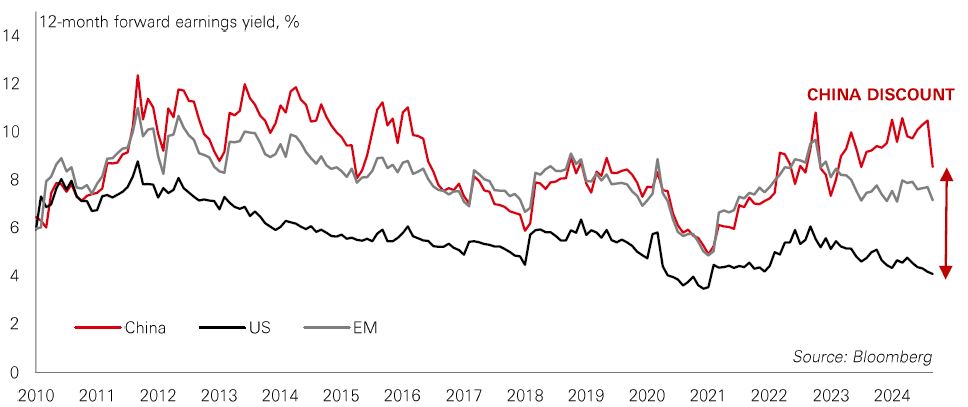

As for markets, many Asian investors remain cautious on Chinese stocks, arguing that it will take a long time for capital flows to return. But at 11.5x earnings, China still trades at a heavy discount to EM (14x) and global stocks (21x). With bad news still in the price, good news could be ‘doubly good’ for stocks.

Another way to think about market effects is that China’s stimulus sets up a rotation trade in global stocks. China’s rally has already caused volatility in regional fund flows, affecting markets like India, South Korea, and Japan.

Geopolitical risks have been on the rise in 2024 – but the first question might be, “so what?”. Many investors already feel well-equipped to deal with geopolitical risks. Most of the time, after all, the “geopolitical risk premium” has only a fleeting or transitory influence on investment markets. The effects unwind fairly quickly.

But this time could be different. There are several reasons why investors need to take geopolitics seriously in their asset allocation considerations. First, economic power is diffusing to Asia and the Global South, with profound implications for the macro-economy and the financial system. Second, the global environment has become less friendly to international cooperation. And third, the policies and principles that have stabilised the global order over the last 30 to 40 years seem increasingly obsolete.

It means that the “nice” economic regime now risks being “vile” – or, to spell it out, one of “Volatile Inflation and Limited Expansion”. If left unchecked, it implies rising prices and lower economic growth potential. For investors, portfolio strategy will need to be prepared for such an eventuality and resilient to the implications of shorter business cycles, greater market dispersion, and changed correlations.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice.

Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 11.00am UK time 18 October 2024.

At its October meeting, the European Central Bank (ECB) delivered its second rate cut in as many months and its third of this easing cycle. During the summer, the expectation was that it would cut at a pace of 0.25% every other meeting. What has changed? One factor is that the Federal Reserve has become more willing to ease policy. However, there have also been important eurozone developments. First, the latest inflation numbers show tentative signs that service sector inflation is now weakening, having been relatively sticky earlier this year. Wage growth is also softening, supporting the view that inflation pressures are fading. Second, activity data have surprised to the downside – the PMIs point to a deceleration in growth during H2 2024, led by Germany.

With the inflation situation improving, growth looking patchy – particularly in Germany – and the ECB easing policy at a brisker pace, Bunds have been outperforming US Treasuries since mid-September, reversing the trend seen since mid-April.

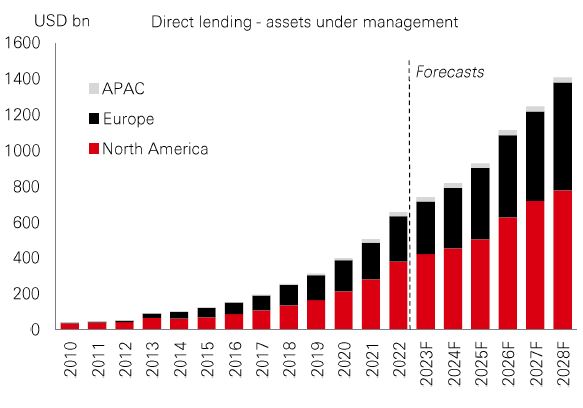

The private credit market has grown rapidly in recent years, driven in part by strong demand for direct lending. There have been two key reasons for this: one is that traditional banks have retrenched from parts of the lending market, leaving private credit managers to fill the void. Another is that direct lending proved popular with private equity managers during the post-Covid deal-making boom.

For private credit investors, the returns have been strong. With an average yield of nearly 12%, the asset class has outperformed other Credits. With the global easing cycle underway, returns are expected to moderate over time, but it’s expected to remain a high yield asset class.

While North America and Europe currently dominate the direct lending markets, Asia is comparatively small – but growing strongly in some areas. With around 80% of total credit in Asia still provided by banks, there is growing demand for alternative sources of finance for fast-growing firms, mergers and acquisitions, and private equity deals.

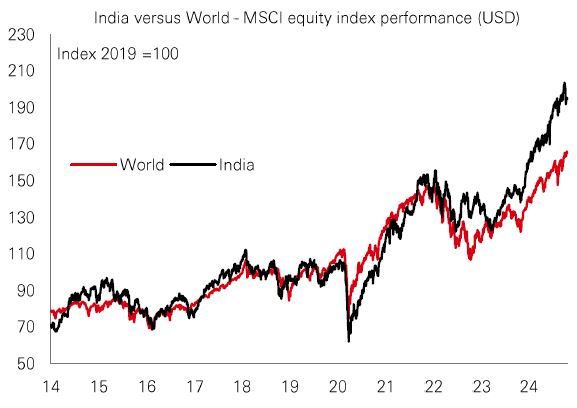

Reforms implemented over the past decade along with more credible monetary and fiscal policy have allowed India to begin tapping its catch-up potential and enviable demographics. The IMF expects India to be the fastest growing G20 economy over the remainder of the decade, with real GDP rising by almost 50% by 2029.

Consistent with the recent strong and expected growth, MSCI India has outperformed MSCI ACWI by a significant margin over the last five years. Importantly, however, the Indian equity market now offers greater diversification and less volatility than in the past – MSCI India now comprises over 150 stocks versus under 80 in late 2019. Moreover, it is not just in the equity space that India stands out – its 10y government yield is among the highest for investment grade issuers and has a low correlation with global bonds. Add in an undervalued INR, which also exhibits less volatility than the average EM currency, and there is a strong case for India to be viewed as an asset class in its own right, rather than simply part of a benchmark.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice.

Source: HSBC Asset Management. Macrobond, Bloomberg, Datastream, Preqin. Data as at 11.00am UK time 18 October 2024.

Source: HSBC Asset Management. Data as at 7.30am UK time 18 October 2024. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice.

A solid increase in US retail sales during September buoyed US Treasury yields towards the end of last week. In stocks, the small-cap Russell 2000 saw the strongest gains, with the large-cap S&P 500 touching new highs, helped by upbeat Q3 earnings news. In Europe, the ECB cut rates by 0.25%, noting that inflation was increasingly under control but warning the outlook for the bloc’s economy was worsening. In Asia, Chinese equities pulled back for a second week following recent rallies, with a slew of macro data releases and policy expectations remaining in focus. India’s Sensex also fell, but some ASEAN markets fared better, with Thai and Indonesian equities ending positively. Brazil’s Ibovespa and Mexico’s IPC were also both on course to finish higher. Elsewhere, the oil price fell on easing fears over tensions in the Middle East. Gold once again reached new highs.

This document has been issued by The Hongkong and Shanghai Banking Corporation Limited (the "Bank") in the conduct of its regulated business in Hong Kong and may be distributed in other jurisdictions where its distribution is lawful. It is not intended for anyone other than the recipient. The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document must not be distributed to the United States, Canada or Australia or to any other jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings.

This document has no contractual value and is not and should not be construed as an offer or the solicitation of an offer or a recommendation for the purchase or sale of any investment or subscribe for, or to participate in, any services. The Bank is not recommending or soliciting any action based on it.

The information stated and/or opinion(s) expressed in this document are provided by HSBC Global Asset Management Limited. We do not undertake any obligation to issue any further publications to you or update the contents of this document and such contents are subject to changes at any time without notice. They are expressed solely as general market information and/or commentary for general information purposes only and do not constitute investment advice or recommendation to buy or sell investments or guarantee of returns. The Bank has not been involved in the preparation of such information and opinion. The Bank makes no guarantee, representation or warranty and accepts no responsibility for the accuracy and/or completeness of the information and/or opinions contained in this document, including any third party information obtained from sources it believes to be reliable but which has not been independently verified. In no event will the Bank or HSBC Group be liable for any damages, losses or liabilities including without limitation, direct or indirect, special, incidental, consequential damages, losses or liabilities, in connection with your use of this document or your reliance on or use or inability to use the information contained in this document.

In case you have individual portfolios managed by HSBC Global Asset Management Limited, the views expressed in this document may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management Limited primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

The information contained within this document has not been reviewed in the light of your personal circumstances. Please note that this information is neither intended to aid in decision making for legal, financial or other consulting questions, nor should it be the basis of any investment or other decisions. You should carefully consider whether any investment views and investment products are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. The investment decision is yours but you should not invest in any product unless the intermediary who sells it to you has explained to you that the product is suitable for you having regard to your financial situation, investment experience and investment objectives. The relevant product offering documents should be read for further details.

Some of the statements contained in this document may be considered forward-looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Such statements do not represent any one investment and are used for illustration purpose only. Customers are reminded that there can be no assurance that economic conditions described herein will remain in the future. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We can give no assurance that those expectations reflected in those forward-looking statements will prove to have been correct or come to fruition, and you are cautioned not to place undue reliance on such statements. We do not undertake any obligation to update the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Investment involves risk. It is important to note that the capital value of investments and the income from them may go down as well as up and may become valueless and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Past performance information may be out of date. For up-to-date information, please contact your Relationship Manager.

Investment in any market may be extremely volatile and subject to sudden fluctuations of varying magnitude due to a wide range of direct and indirect influences. Such characteristics can lead to considerable losses being incurred by those exposed to such markets. If an investment is withdrawn or terminated early, it may not return the full amount invested. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability in certain jurisdictions. Narrowly focused investments and smaller companies typically exhibit higher volatility. There is no guarantee of positive trading performance. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Mutual fund investments are subject to market risks. You should read all scheme related documents carefully.

Copyright © The Hongkong and Shanghai Banking Corporation Limited 2024. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Issued by The Hongkong and Shanghai Banking Corporation Limited