25 November 2024

Over the previous week, risk markets have paused for breath. US stocks have unwound some of their big post-election gains, high-yield credit spreads have picked up from multi-year lows, and commodity prices have lost ground.

We think recent market action reflects a new reality facing investors. There is a “tug of war” between enthusiasm around significant aspects of the US policy outlook – mainly deregulation and tax cuts – versus concerns about the potentially stagflationary effects of loose fiscal policy and an acceleration of the trend in US isolationism.

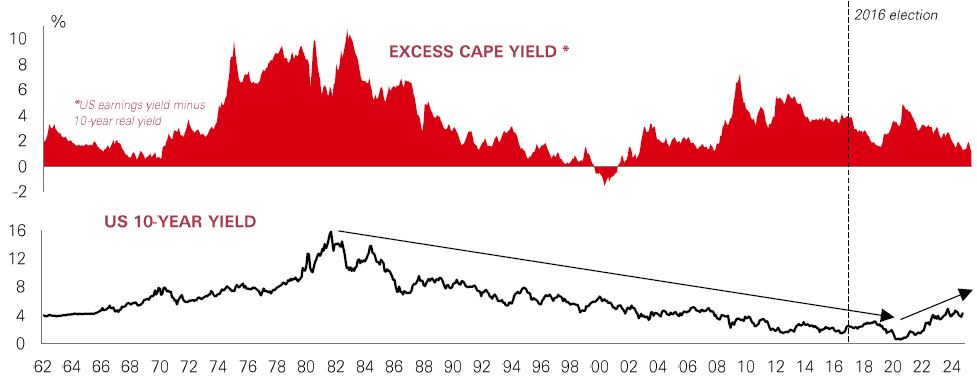

US 10-year yields are hovering just below April’s year-to-date highs despite the Fed now in easing mode and inflation in a holding pattern, with room for more disinflation in 2025. This is because there is now much greater uncertainty around the inflation outlook, reflected in the recent pick-up in the US term premium.

Structurally higher inflation and interest rates pose many challenges for investment markets. It weighs on the growth and earnings outlook. And it makes stock valuations less attractive versus bonds. The most expensive parts of the stock market such as US mega-cap tech – which look priced for perfection – could be vulnerable.

Four years after being badly hit by Covid travel restrictions, air traffic has finally caught up with 2019 levels – but the global aviation industry’s cyclical and structural growth drivers are changing.

A new research explores the sector’s investment outlook – with a focus on airports, which are a key part of the infrastructure asset class. Overall demand looks robust, but new trends in the traveller ‘mix’ and geographic growth are emerging. While business travel continues to decline, demand from cohorts travelling for leisure and ‘visiting friends and relatives’ is growing quickly. And in terms of regional demand, industry forecasts suggest that fast-growing developing nations will contribute 85% of the industry’s growth over the next 20 years – with Asia Pacific expected to be a powerhouse.

For airport investors, post-pandemic challenges are giving way to new opportunities, with wealth and demographic trends expected to drive above-GDP growth rates for the industry. Together with offering a wider range of travel destinations, there are opportunities for airports to enhance returns with a wider range of premium services.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. Diversification does not ensure a profit or protect against loss.

Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 7.30am UK time 22 November 2024.

With Q3 earnings season drawing to a close in the US, last week saw results from the market’s most closely-watched technology giant, NVIDIA. Like the rest of the S&P 500’s ‘Magnificent 7’ tech stocks, NVIDIA’s quarterly profits were ahead of analyst forecasts for the quarter. Indeed, with more than 90% of companies in the index having reported, around 75% of them have beaten profit expectations.

However, the scale of index-wide profits beats – averaging about 4.3% above estimates, according to Factset – is roughly half that of their 5-year average. Firms may be finding it harder to beat forecasts. And given the index trades on a price-to-earnings ratio of 22.3x (versus its 15-year average of 16.4x), prices could be vulnerable if future earnings disappoint. The communication services, IT and healthcare sectors have seen the largest (aggregate) beats, while energy and materials have seen the largest (aggregate) misses.

From here, profit growth expectations remain high into 2025. But against a backdrop of policy uncertainty and a cooling economy, any weakness could lead to heightened volatility.

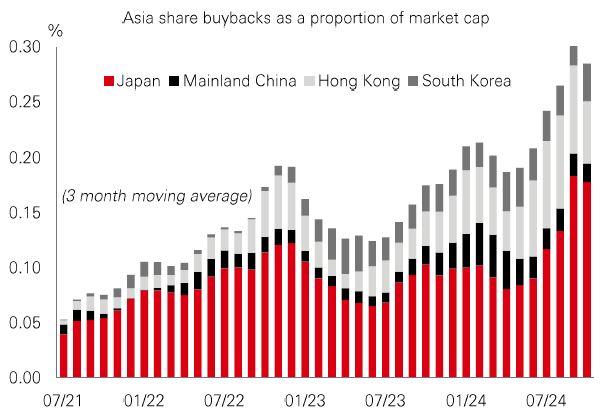

US stock buybacks have boomed in recent years as companies looked to boost earnings-per-share, buoy their valuations, and allocate cash to reward shareholders. Against a backdrop of falling rates – dampening returns on cash holdings – this popularity should persist. But this isn’t just a US phenomenon – Asia stock markets have seen a buyback boost too.

A key difference in Asia is that buybacks have been driven by regional efforts to improve corporate governance. Governments have called on firms to be more investor-friendly and improve their valuations. Japan is a prime example, and is now seeing a third consecutive year of record buybacks in 2024. A similar move in South Korea – the ‘Value-Up’ programme – saw a 25% rise in buybacks in H1-24 from H1-23. Mainland Chinese authorities have also demanded action on profitability and shareholder returns. Share repurchases there are on course to break domestic records this year, with September’s stimulus measures including a RMB300bn relending facility earmarked specifically for share buybacks. With Asian markets on undemanding valuations, further progress on corporate reforms and share buybacks could provide upside.

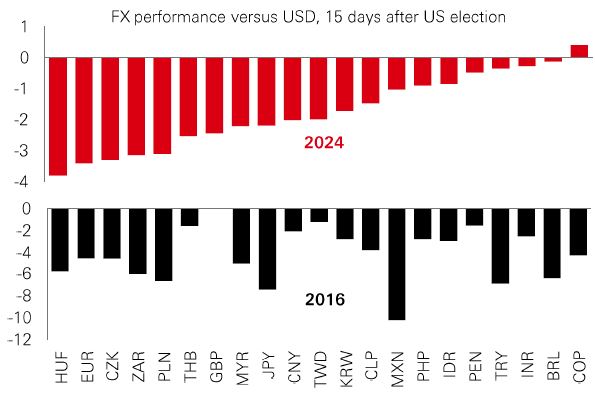

Recent action with the US dollar looks to be following the 2016 playbook. The DXY index or “dixie” is up around 3-4% since the US election, about the same as in the 15 days following the 2016 poll.

But moves in individual FX pairs show some interesting differences versus the 2016 experience. The most striking contrast is the Mexican peso. This was one of 2016’s biggest casualties, and although it’s down this time around, it is one of the better performers. Other Latin American currencies have held up well too – the Brazilian real and Columbian peso have hardly budged. This resilience could reflect a hawkish tilt to central bank policymaking in the region in recent months.

Moves in Europe have also been quite different. The euro and some Eastern European currencies have been badly hit by the election result. Trade tariffs would come at a very difficult time for the region’s manufacturers. But the good news is FX weakness supports external competitiveness for export-dependent firms. In 2025, US-specific factors – policy and inflation trends – are likely to be a big influence on the dollar. But global economic and political developments will also be key.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice.

Source: HSBC Asset Management. Macrobond, Bloomberg, Datastream. Data as at 7.30am UK time 22 November 2024.

Source: HSBC Asset Management. Data as at 7.30am UK time 22 November 2024. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice.

Risk markets were resilient despite heightened geopolitical tensions, with both oil and gold prices rallying. The US DXY dollar index paused for breath after its recent strong run. Core government bonds consolidated ahead of key US inflation data and mixed comments from Fed officials. US equities saw a broad-based rally as investors digested Q3 earnings. The Euro Stoxx index fell modestly, while Japan’s Nikkei 225 weakened as the yen rebounded versus the US dollar. BoJ governor Ueda reiterated his commitment to gradual rate hikes. Emerging market stock markets were mixed. The Shanghai Composite and Hang Seng indices finished the week lower, but the tech-driven South Korea Kospi index performed well. India’s Sensex index fell further. In Latin America, Brazil’s Bovespa and Mexico’s IPC equity indices were on the defensive. Meanwhile, copper was little changed.

This document has been issued by The Hongkong and Shanghai Banking Corporation Limited (the "Bank") in the conduct of its regulated business in Hong Kong and may be distributed in other jurisdictions where its distribution is lawful. It is not intended for anyone other than the recipient. The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document must not be distributed to the United States, Canada or Australia or to any other jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings.

This document has no contractual value and is not and should not be construed as an offer or the solicitation of an offer or a recommendation for the purchase or sale of any investment or subscribe for, or to participate in, any services. The Bank is not recommending or soliciting any action based on it.

The information stated and/or opinion(s) expressed in this document are provided by HSBC Global Asset Management Limited. We do not undertake any obligation to issue any further publications to you or update the contents of this document and such contents are subject to changes at any time without notice. They are expressed solely as general market information and/or commentary for general information purposes only and do not constitute investment advice or recommendation to buy or sell investments or guarantee of returns. The Bank has not been involved in the preparation of such information and opinion. The Bank makes no guarantee, representation or warranty and accepts no responsibility for the accuracy and/or completeness of the information and/or opinions contained in this document, including any third party information obtained from sources it believes to be reliable but which has not been independently verified. In no event will the Bank or HSBC Group be liable for any damages, losses or liabilities including without limitation, direct or indirect, special, incidental, consequential damages, losses or liabilities, in connection with your use of this document or your reliance on or use or inability to use the information contained in this document.

In case you have individual portfolios managed by HSBC Global Asset Management Limited, the views expressed in this document may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management Limited primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

The information contained within this document has not been reviewed in the light of your personal circumstances. Please note that this information is neither intended to aid in decision making for legal, financial or other consulting questions, nor should it be the basis of any investment or other decisions. You should carefully consider whether any investment views and investment products are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. The investment decision is yours but you should not invest in any product unless the intermediary who sells it to you has explained to you that the product is suitable for you having regard to your financial situation, investment experience and investment objectives. The relevant product offering documents should be read for further details.

Some of the statements contained in this document may be considered forward-looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Such statements do not represent any one investment and are used for illustration purpose only. Customers are reminded that there can be no assurance that economic conditions described herein will remain in the future. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We can give no assurance that those expectations reflected in those forward-looking statements will prove to have been correct or come to fruition, and you are cautioned not to place undue reliance on such statements. We do not undertake any obligation to update the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Investment involves risk. It is important to note that the capital value of investments and the income from them may go down as well as up and may become valueless and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Past performance information may be out of date. For up-to-date information, please contact your Relationship Manager.

Investment in any market may be extremely volatile and subject to sudden fluctuations of varying magnitude due to a wide range of direct and indirect influences. Such characteristics can lead to considerable losses being incurred by those exposed to such markets. If an investment is withdrawn or terminated early, it may not return the full amount invested. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability in certain jurisdictions. Narrowly focused investments and smaller companies typically exhibit higher volatility. There is no guarantee of positive trading performance. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Mutual fund investments are subject to market risks. You should read all scheme related documents carefully.

Copyright © The Hongkong and Shanghai Banking Corporation Limited 2024. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Issued by The Hongkong and Shanghai Banking Corporation Limited