23 December 2024

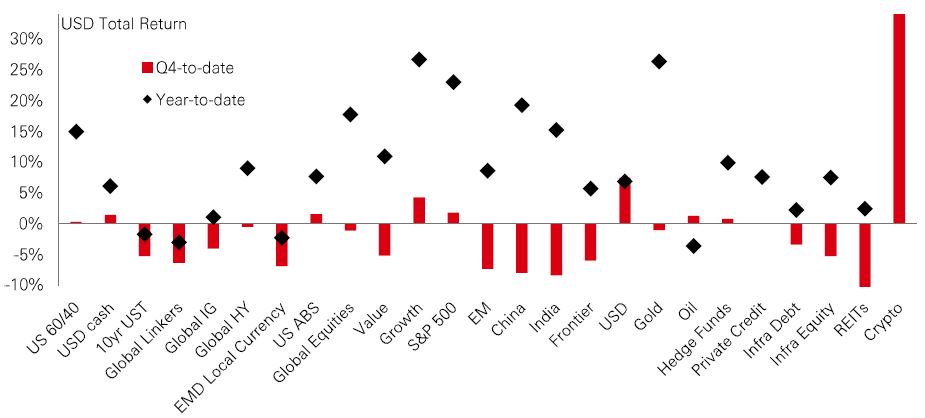

The story of investment markets in 2024 has been dominated by the course of disinflation and the global rate-cutting cycle. Last week’s sell-off in global stocks on a more hawkish Fed outlook showed how hyper-sensitive markets are to disappointing macro news. But Q4 has delivered some extra twists and turns, including the outcome of the US presidential election. The result raised uncertainty over future US policy, spurred strong moves in global risk assets, and drove a rally in the US dollar. It even got some credit for a surge in the price of cryptocurrencies.

In stocks, the strongest momentum has been in US large caps, especially in tech-related sectors. Despite last week’s moves, the S&P 500 is still up in Q4 (and up by more than 20%+ this year). Growth has thrived while value has lagged. But it was emerging market equities – which have been strong in 2024 – that felt the most pain in Q4 (see Page 2).

In fixed income, the potential for inflationary policy and higher-for-longer rates saw US Treasury yields rise. In credit, High Yield and ABS were more muted in Q4 (but have been strong in 2024 overall). Meanwhile in alternative assets, Q4 was weak but diversifiers like hedge funds, private credit, and real estate are on course to finish the year positively.

So, what comes next? We think that active fiscal policy, trade uncertainty, and geopolitical tensions may cause volatility and could leave investors ‘spinning around’ in 2025. And despite the moves in Q4, there is scope for performance to broaden out to developed markets beyond North America, as well as emerging and frontier markets next year (see Market Spotlight).

Overall market returns in 2024 are on track to be very solid. The good news for investors heading into next year is that global growth remains resilient, AI is driving revenue growth (and economic productivity), and central banks are still expected to cut rates. But could signs of inflation persistence force a more gradual easing path? This would pose obvious challenges to market performance, reflected in last week’s Fed-induced market wobble. The most expensive parts of the market (US tech) – which look priced for perfection – could be vulnerable, especially if profits disappoint.

If the US market starts to struggle, can other regions take the lead? Many markets outside of the US benefit from favourable valuations and improving profit growth. But for most EMs, a lot will depend on the course of the US dollar, the potency of China policy easing, and developments around trade policy. And for Europe, can the politics tilt in a more investor-friendly direction? Fiscal policy developments in France and Germany will be important.

Finally, could a pickup in market volatility support the performance of defensive sectors - healthcare, staples, utilities – that have lagged this year? With these sectors also acting as “bond proxies”, the direction of rates will also matter.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way.

Source: HSBC Asset Management. Macrobond, Bloomberg. Data as at 7.30am UK time 20 December 2024.

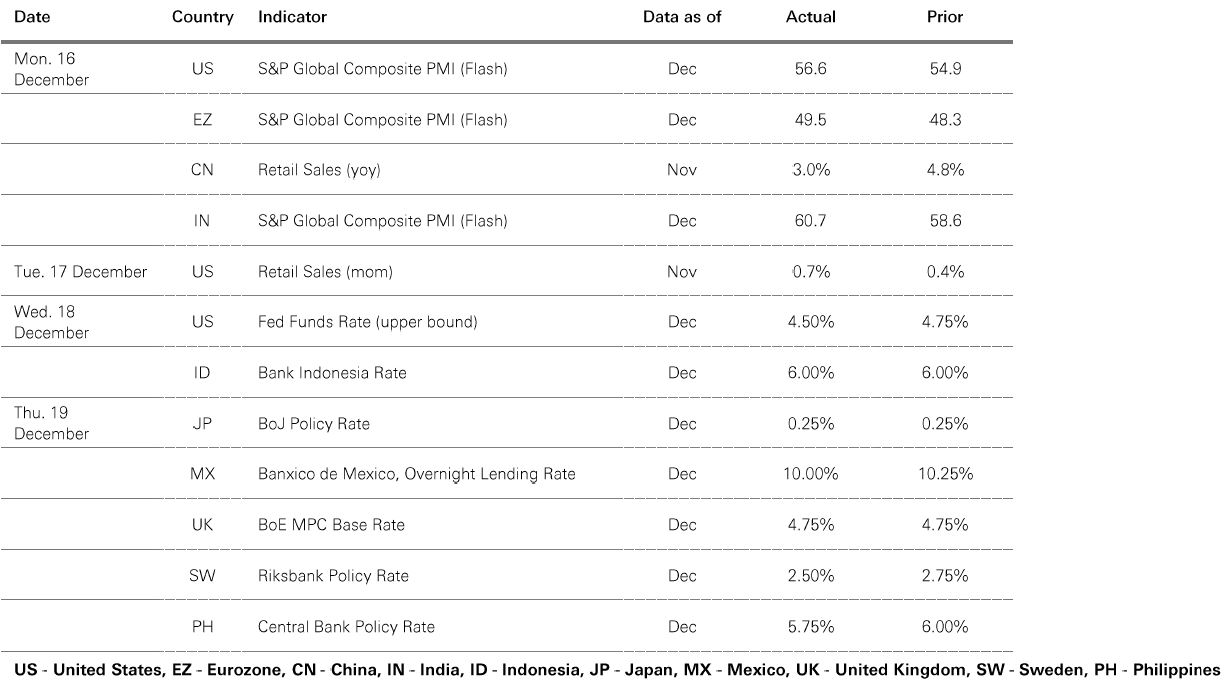

The Fed cut rates as expected at its December meeting but the FOMC’s revised projections unsettled markets. Upward revisions to inflation resulted in the removal of two rate cuts in 2025 – the Fed now expects to reduce the funds rate by 0.5% next year, rather than 1%. Chair Powell noted that following a sticky patch in recent months, evidence that inflation was again moving towards target would be needed before the Fed sanctions another cut. A pause in early 2025 looks likely.

Treasury yields jumped by over 0.1% and the USD hit its highest level since 2022 as markets moved to price in a slower pace of policy easing. But the biggest move came in equities – the S&P 500 fell 3% on the day.

The market is now pricing in a very shallow slope for policy easing – only 1-2 cuts in 2025. Combined with significant Treasury issuance, this has pushed the 10yr yield back above 4.50%. This maintains a solid income component for fixed income investors. And on a cyclical basis, if inflation were to decline more quickly than expected – possible given its hitherto bumpy path – or growth disappoints, Treasury yields could fall back.

Stock markets in emerging and frontier economies have delivered a broadly positive performance in 2024 – but Q4 has been difficult.

In part, recent weakness is down to the headwind of a resurgent US dollar, which has rallied since early October. Concerns over higher-for-longer US rates and heightened trade tensions have added to the woes. These factors have complicated an already challenging domestic backdrop for Latam countries like Brazil. And together with a weak profits outlook, that led to a big decline for the region’s stocks in Q4.

Policy uncertainty has also dragged on markets in EM ASEAN, where financial stocks (which have a high weighting in regional indices) have weakened. Mainland Chinese stocks have also lost ground in Q4. But year-to-date, mainland China, together with Taiwan and India, remains among the strongest EM performers this year. Even excluding mainland China, the benefit of idiosyncratic trends and strong structural growth stories have helped broader EM, Asia, and Frontier stock universes to perform well in 2024.

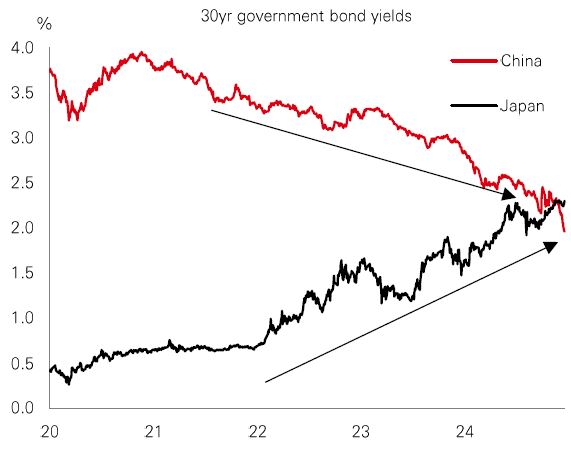

In recent weeks, China’s longer-dated government bond yields have fallen below those of Japan, in a historic shift that reflects significant developments in both economies.

The global inflation shock boosted Japanese nominal GDP and appears to have triggered a “virtuous cycle” in wages and prices. While the BoJ opted not to hike at its December meeting, markets expect 0.4%-0.5% of tightening in 2025. This move away from deflation, the expectation of gradual policy normalisation, and higher US Treasury yields, have combined to push longer-dated Japanese yields higher.

In contrast, Chinese bond yields have trended lower since the pandemic, reflecting a period of weak inflation, lingering growth concerns, and ongoing PBOC easing expectations. December’s Politburo meeting called for “moderately loose” monetary policy, pointing to further rate cuts.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. Diversification does not ensure a profit or protect against loss. Source: HSBC Asset Management. Macrobond, Bloomberg, Datastream. Data as at 7.30am UK time 20 December 2024.

Source: HSBC Asset Management. Data as at 7.30am UK time 23 December 2024. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice.

The US Fed lowered rates by 0.25% last week, but a more hawkish outlook from the FOMC caused a spike in market volatility, with government bond yields moving higher and risk assets selling off. US 10yr Treasuries jumped above 4.5% – their highest level since May – in response to revised rate expectations, with the US dollar also rallying against a basket of major currencies. In stocks, the S&P 500 led global indices lower mid-week, with the small-cap Russell 2000 falling sharply, and Europe’s Stoxx 600 index also losing ground. In emerging markets, China’s Shanghai Composite withstood the worst of the volatility with only modest declines, while India’s Sensex, Brazil’s Bovespa and Mexico’s IPC all saw sharper losses. In commodities, the WTI oil price was down modestly through last week, while gold and copper prices also fell.

This document has been issued by The Hongkong and Shanghai Banking Corporation Limited (the "Bank") in the conduct of its regulated business in Hong Kong and may be distributed in other jurisdictions where its distribution is lawful. It is not intended for anyone other than the recipient. The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document must not be distributed to the United States, Canada or Australia or to any other jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings.

This document has no contractual value and is not and should not be construed as an offer or the solicitation of an offer or a recommendation for the purchase or sale of any investment or subscribe for, or to participate in, any services. The Bank is not recommending or soliciting any action based on it.

The information stated and/or opinion(s) expressed in this document are provided by HSBC Global Asset Management Limited. We do not undertake any obligation to issue any further publications to you or update the contents of this document and such contents are subject to changes at any time without notice. They are expressed solely as general market information and/or commentary for general information purposes only and do not constitute investment advice or recommendation to buy or sell investments or guarantee of returns. The Bank has not been involved in the preparation of such information and opinion. The Bank makes no guarantee, representation or warranty and accepts no responsibility for the accuracy and/or completeness of the information and/or opinions contained in this document, including any third party information obtained from sources it believes to be reliable but which has not been independently verified. In no event will the Bank or HSBC Group be liable for any damages, losses or liabilities including without limitation, direct or indirect, special, incidental, consequential damages, losses or liabilities, in connection with your use of this document or your reliance on or use or inability to use the information contained in this document.

In case you have individual portfolios managed by HSBC Global Asset Management Limited, the views expressed in this document may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management Limited primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

The information contained within this document has not been reviewed in the light of your personal circumstances. Please note that this information is neither intended to aid in decision making for legal, financial or other consulting questions, nor should it be the basis of any investment or other decisions. You should carefully consider whether any investment views and investment products are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. The investment decision is yours but you should not invest in any product unless the intermediary who sells it to you has explained to you that the product is suitable for you having regard to your financial situation, investment experience and investment objectives. The relevant product offering documents should be read for further details.

Some of the statements contained in this document may be considered forward-looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Such statements do not represent any one investment and are used for illustration purpose only. Customers are reminded that there can be no assurance that economic conditions described herein will remain in the future. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We can give no assurance that those expectations reflected in those forward-looking statements will prove to have been correct or come to fruition, and you are cautioned not to place undue reliance on such statements. We do not undertake any obligation to update the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Investment involves risk. It is important to note that the capital value of investments and the income from them may go down as well as up and may become valueless and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Past performance information may be out of date. For up-to-date information, please contact your Relationship Manager.

Investment in any market may be extremely volatile and subject to sudden fluctuations of varying magnitude due to a wide range of direct and indirect influences. Such characteristics can lead to considerable losses being incurred by those exposed to such markets. If an investment is withdrawn or terminated early, it may not return the full amount invested. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability in certain jurisdictions. Narrowly focused investments and smaller companies typically exhibit higher volatility. There is no guarantee of positive trading performance. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Mutual fund investments are subject to market risks. You should read all scheme related documents carefully.

Copyright © The Hongkong and Shanghai Banking Corporation Limited 2024. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Issued by The Hongkong and Shanghai Banking Corporation Limited